@AamerMalik-

So I went ahead and put a sample together. The more I thought about it, the more I didnt like my initial solution. While it would work, I really didnt like this part.

FILTER ( ALL ( FactDailyData ),

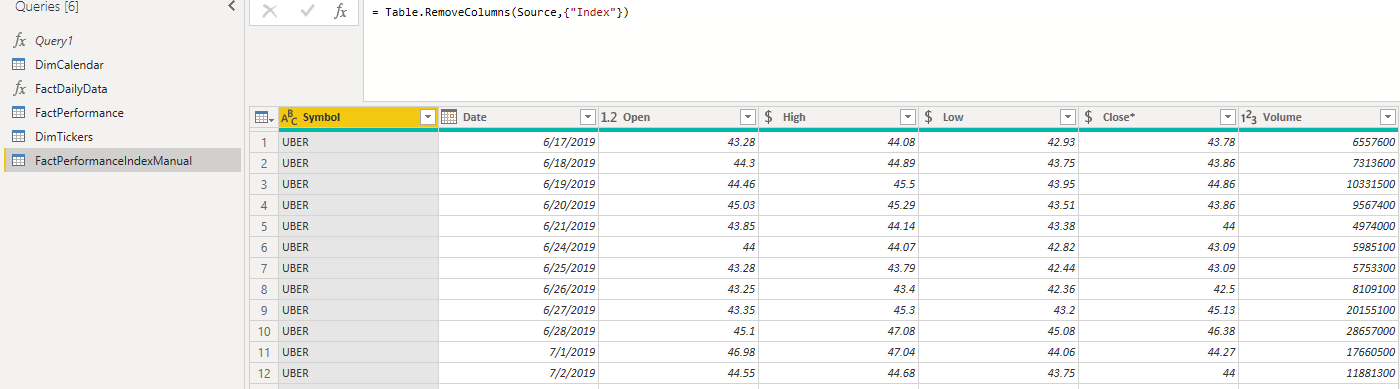

But first things first, getting the index column for each stock. In the attached PBIX file you will see a few tables and couple functions in PQ. Focusing on the “FactPerformanceIndexManual” for the time being. There is a list of stocks (it will reference a different table where I already have the Index, so I need to remove that to get a “clean slate”)

We then sorted by Symbol and then by Date Ascending. Then group the rows by Symbol and aggregate by all data. Now, we need to add something to the end of generated M code:

This will tell PQ to keep the order that we had set eariler for each grouping. So we have:

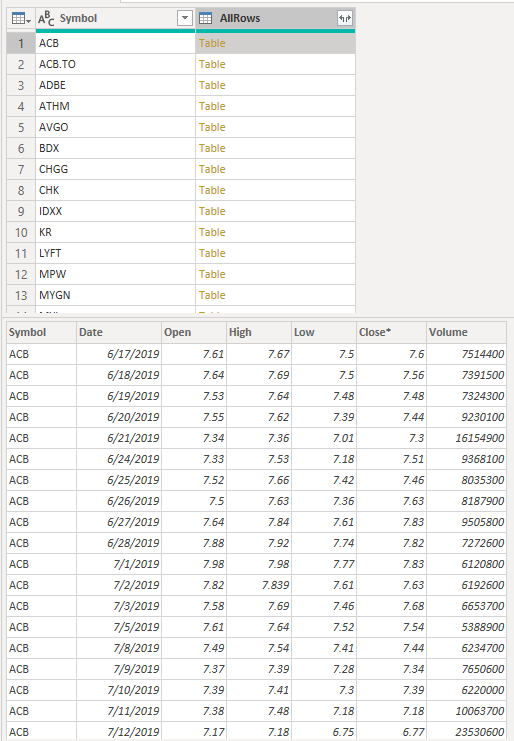

Now add a custom column with the following to get an Index for each sub table:

Table.AddIndexColumn(

[AllRows],"Index",1,1)

Its the same code that would be generated from the Add Column–>Index Column toolbar, with the exception we add in our [AllRows] as the table, so that PQ will restart the count at each table. Remove all the other columns except this last one and set data types and you are all set:

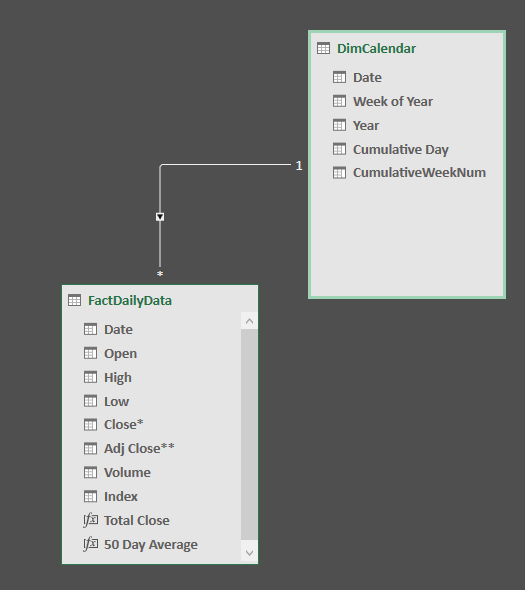

Load that, along with your calendar table and should have Dimension table for your Tickers as well. Data model looks like:

With Dates on rows from our DimCalendar Table, and Symbol (from DimTickers) as a slicer (or could be whatever) we can use the following function. I put comments in the code.

"X" Day Average =

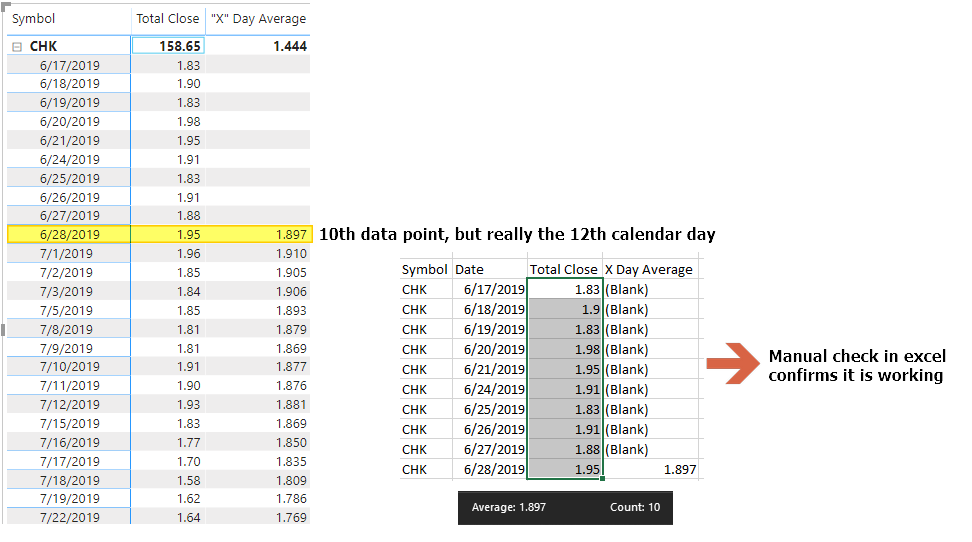

Var _Length=10

/*This gives the total count of rows for each stock up until the current date

want to be sure we have enough data points to generate a correct MA*/

Var _PerformanceCount=

CALCULATE(

COUNTROWS( FactPerformance ),

FILTER(

ALL( DimCalendar),

MAX(DimCalendar[Date]) >= DimCalendar[Date]

)

)

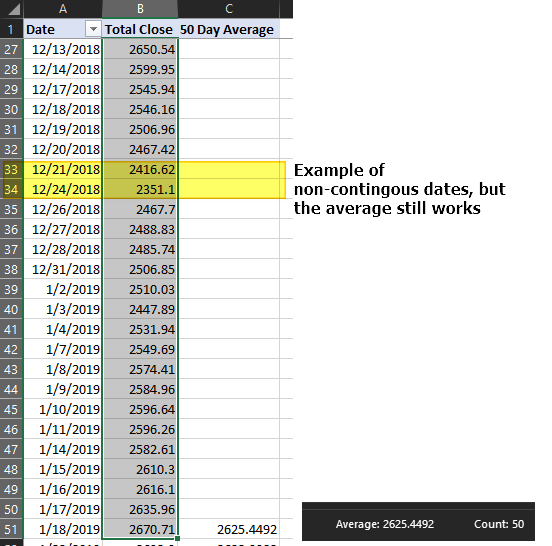

/*Since we cannot use simply 10 days, we need to figure out what the date is of the

10th day.

-We want to lookup the Date of the 10th day back in the Fact table

-In that table, we go to the Index column and want to find where index is equal to the

length +1. We add one so that we count the current day

-Then we want to be sure we have the correct symbol

-This then gives us what the date was of the 10th day back*/

Var _BeginDate =

LOOKUPVALUE(

FactPerformance[Date]

,FactPerformance[Index],_PerformanceCount - _Length +1

,FactPerformance[Symbol], SELECTEDVALUE(DimTickers[Symbol])

)

/*What the current date is in the currnt filter context*/

VAR _CurrentDate= MAX( DimCalendar[Date])

RETURN

IF(

_PerformanceCount >= _Length --This checks to be sure we have enough data points

&&

NOT ISBLANK([Total Close]), --This checks to be sure we have a close on that date

CALCULATE( --Calculate is the only thing that can change the filter context

[Avg Close], --Just a simple Average(Fact[Close])

DATESBETWEEN( --DatesBetween returns a table of dates from start and end date

DimCalendar[Date] --Dates Columns

,_BeginDate --StartDate is our begin date variable from above

,_CurrentDate --EndDate is just the current date in the current filter context

)

)

)

This is just a “bonus”, but there’s a function in the file that will go out to yahoo finance and get the historical data for a list of tickers:

(Ticker) =>

let

Source =

Web.Page(

Web.Contents(

"https://finance.yahoo.com/quote/"

&Ticker

&"/"

&"history?p="

&Ticker

)

),

Data2 = Source{2}[Data],

#"Changed Type" = Table.TransformColumnTypes(Data2,{{"Date", type date}, {"Open", type number}, {"High", type number}, {"Low", type number}, {"Close*", type number}, {"Adj Close**", type number}, {"Volume", type number}}),

#"Sorted Rows" = Table.Sort(#"Changed Type",{{"Date", Order.Ascending}}),

#"Added Index" = Table.AddIndexColumn(#"Sorted Rows", "Index", 1, 1)

in

#"Added Index"

And in this function it already does the Index from above. But that was just more for me and just seeing what can be in PQ, so probably not needed for your case as you probably have a data source already.

Let me know what you think.

Moving Aveage, Based on data not # of actual days.pbix (265.4 KB)